Florida Roof Insurance Claims: Step‑by‑Step Guide (Documentation, Timeline, Mistakes)

Imagine a storm just came through, and you’ve walked around the outside of your house, looked up at the roof from the yard, and something doesn’t look right.

Maybe a few tiles are gone. Maybe there’s a dark patch where there wasn’t one before. Maybe you’re not even sure what you’re looking at, but something’s off.

What happens next is where a lot of homeowners in Florida get it wrong.

Not because they’re careless, but because nobody explains how the claims process actually works. Insurance policies are dense, adjusters are busy, and the gap between what you’re owed and what you end up with can be significant if you don’t know what to expect.

This guide is a straight walkthrough. What to do first, what to photograph, how adjusters evaluate damage, how estimates work, what can go wrong, and how to protect yourself at every stage. If you’re in Florida, and especially South Florida, some of this will be more specific to your situation than a generic national guide, because Florida’s insurance market has its own rules, its own challenges, and its own common pitfalls.

If you need help documenting storm damage, contact us and get help before you file. Let’s begin.

Don’t Touch Anything Yet

The instinct after a storm is to clean up. Get the debris off the roof, clear the gutters, and move on. Resist that instinct at least until you’ve thoroughly documented everything.

Once you remove damaged materials, clear debris, or start any kind of cleanup, you are erasing evidence. An adjuster who arrives two days after a storm at a clean property has no way of fully assessing what the storm actually did. They’re working from what they can see, and if you’ve already tidied up, they’ll see less.

There’s one exception: if your roof is actively leaking and water is coming into the living space, you need to act to prevent further damage. That’s what emergency tarping is for. Apply temporary protection, keep all your receipts, and take photos of everything before and after the tarp goes on. Emergency mitigation costs are typically reimbursable under most Florida homeowner policies, but only if you can document what was done and why.

Other than that: document first, clean up second.

Step 1: Document the Damage Thoroughly

This is the most important step in the entire claims process, and the one homeowners most often underdo. Insurance claims are decided on evidence. The quality and completeness of your documentation directly affect the outcome of your claim.

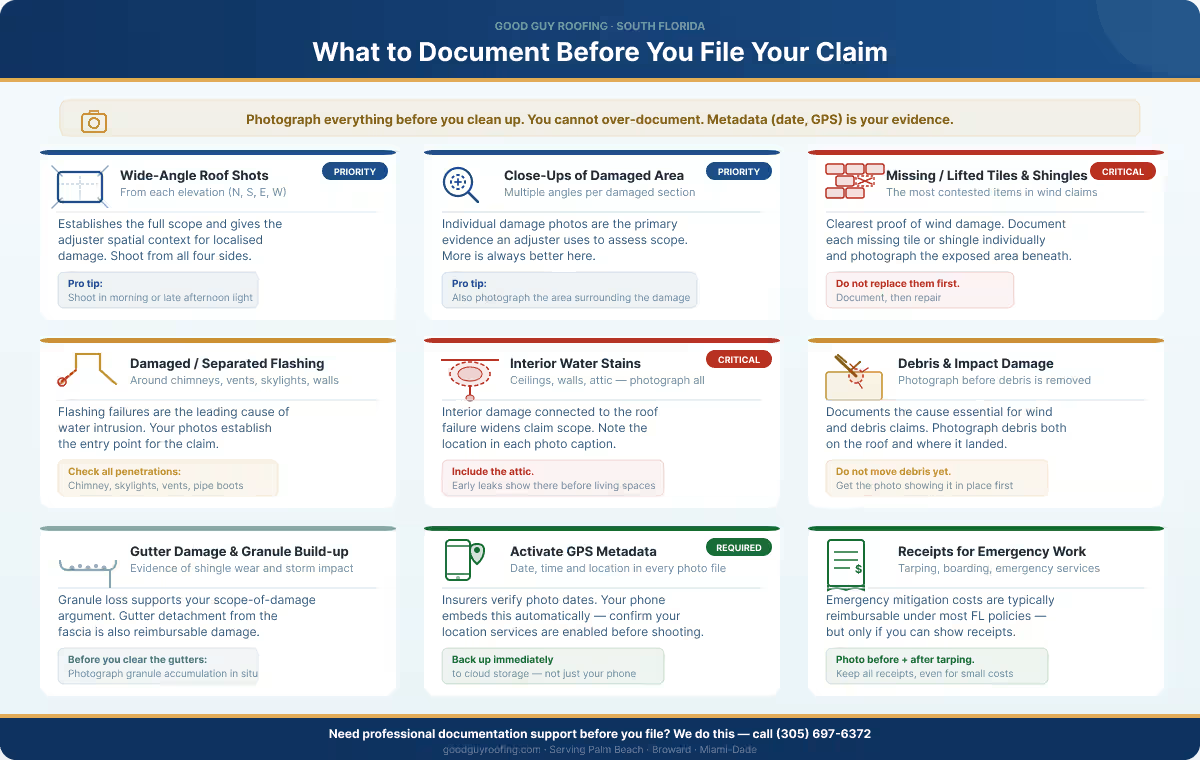

Use your smartphone camera. It’s good enough, and the metadata (date, time, GPS location) is embedded automatically. Take far more photos than you think you need. You cannot over-document. Here’s what to capture:

| What to capture | Why it matters to your claim |

| Wide-angle shots of the full roof from each side | Establishes overall pre-repair condition and gives the adjuster spatial context for localized damage. |

| Close-ups of every damaged area | Individual damage photos are the primary evidence an adjuster uses to assess scope. More is better; you can never over-document. |

| Any missing, lifted, or displaced tiles and shingles | These are the clearest proof of wind damage and the most frequently contested items in claims. |

| Damaged or separated flashing | Flashing failures are a leading cause of water intrusion; photographing them establishes the entry point. |

| Water stains on ceilings, walls, or in the attic | Interior damage that can be connected to the roof failure strengthens the claim and widens its scope. |

| Debris on the roof or ground that caused impact damage | Documenting the cause is essential for wind and debris claims. |

| Gutter damage and any granules in gutters | Granule loss is evidence of shingle degradation caused by impact or wind, supporting the scope-of-damage argument. |

| Dated photographs with GPS metadata active | Insurers will check dates. Metadata on your phone’s photos is timestamped automatically. Confirm this is on. |

| Receipts for any emergency protective measures taken | Tarping, boarding, or other emergency work is typically reimbursable; you need receipts to claim it. |

A few practical notes on documentation. Shoot in good light, ideally early morning or late afternoon, not midday glare. Take each shot from multiple angles. Don’t just photograph the obvious damage; photograph what’s around it as well, so the adjuster can see the extent. And back everything up immediately to cloud storage, not just on your phone.

If you have photos from before the storm, even casual ones that happen to show the roof, pull those together too. Pre-storm documentation is powerful evidence that establishes baseline conditions and makes clear which damage is new.

| Worth knowing:

If you’ve had a professional roof inspection in the past few years, the written report from that inspection is valuable documentation. It establishes the pre-storm condition of your roof in professional terms, which is exactly the baseline an adjuster needs to assess storm damage fairly. This is one of the practical reasons we recommend annual inspections to homeowners: they create a paper trail that matters exactly when you need it most. |

Step 2: Call Your Roofer Before You File

This might feel counterintuitive. Shouldn’t the first call be to the insurance company?

Here’s the case for calling your roofing contractor first: a licensed roofer like Good Guy Roofing can do a professional assessment of your roof, document the damage in technical terms, and give you a clear picture of the scope before you ever talk to an adjuster.

That matters because the scope of damage, how much was affected and what needs to be done, is exactly what the claims process is going to be negotiated around.

Going into a claim armed with a professional assessment puts you in a fundamentally different position than going in with just your own photos and a vague sense that something is wrong. The adjuster knows what they’re doing. You want to know what you’re talking about, too.

Calling your roofer first also means you have someone present when the adjuster comes, which is your right and something you should take advantage of.

After you’ve spoken to your contractor, file the claim. Most Florida policies require you to file promptly after discovering damage, typically within 60 to 72 hours for weather events, though check your specific policy language. Don’t sit on it for a week.

| Schedule an inspection for claim support, and we will document damage professionally |

Step 3: File the Claim and Understand What Happens Next

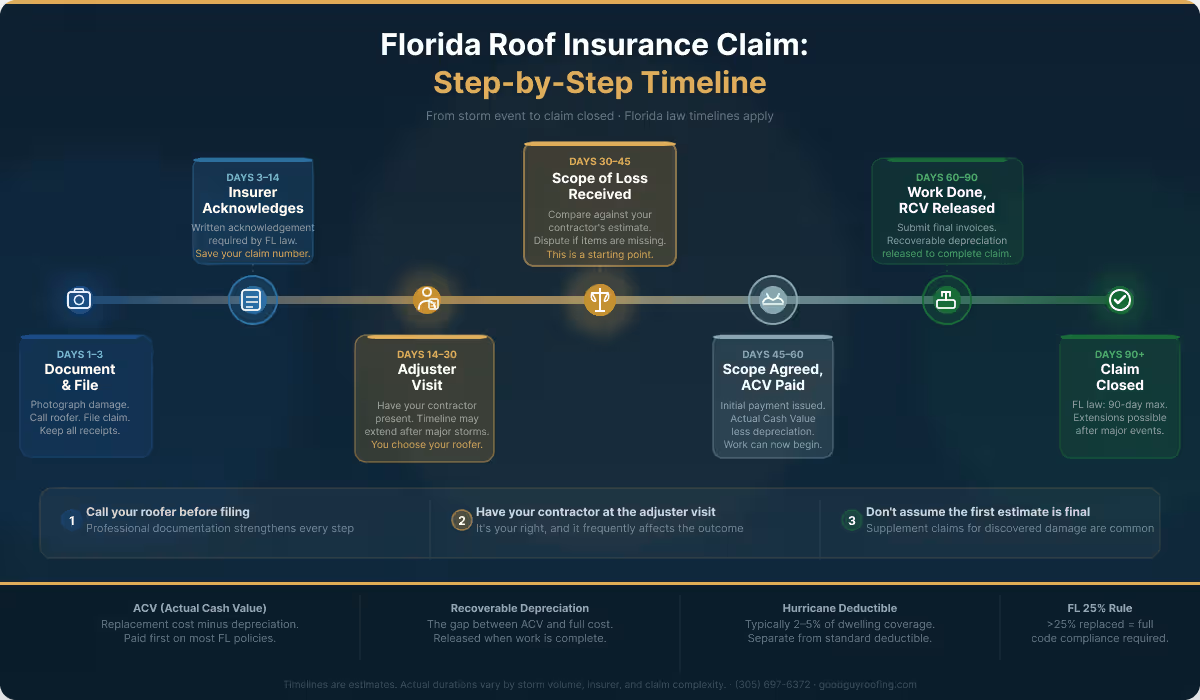

When you file a roof insurance claim in Florida, here’s what the process looks like from the insurer’s side and what you should expect at each stage.

The acknowledgement

Under Florida law, your insurer is required to acknowledge receipt of your claim within 14 days. They should send you a written acknowledgment and assign a claim number. Save that claim number and reference it in every conversation.

The adjuster visit

An adjuster will be assigned to your claim and will contact you to schedule an on-site visit. The timeline for this varies. After a major storm event across South Florida, hurricane or named tropical storm adjusters are working on dozens of properties. You may wait two to three weeks for a visit. After a more localised event, it could be faster.

When the adjuster comes, have your contractor there. Seriously. This is one of the most underused and most valuable things a homeowner can do in this process. A contractor who can point to specific damage, describe it in industry terminology, and explain why it requires repair or replacement carries professional authority that an adjuster will engage with differently than a homeowner saying, “Look, it’s broken.” They’re not adversaries, but they’re speaking the same technical language, and that matters.

Your contractor can also identify damage that an adjuster may miss, particularly damage that isn’t visible from the ground or from a quick roof walk, like lifted tiles that are still in place, flashing separations, or subtle deck damage that only becomes apparent when you know exactly what you’re looking for.

The estimate and scope of work

After the adjuster’s visit, you’ll receive an estimate, sometimes called a scope of loss, that outlines what the insurer believes is covered and what it should cost. This estimate is not a final settlement offer. It’s a starting point.

Compare it against the estimate from your roofing contractor. If there are significant discrepancies, items your contractor identified that the adjuster didn’t include, or cost figures that don’t reflect current South Florida market rates, you can dispute the scope. This is normal, and it happens frequently. After major storm events, the volume of claims means adjuster assessments are sometimes rushed or incomplete.

Document your contractor’s estimate thoroughly. An itemized written estimate from a licensed roofing contractor is one of the strongest tools you have in a scope dispute.

Actual Cash Value vs Replacement Cost Value

This is a distinction that catches people off guard. Many Florida policies pay out Actual Cash Value (ACV) first, which is the replacement cost minus depreciation. On an aging roof, that depreciation can be substantial. The remainder, called the Recoverable Depreciation, is released once the repair or replacement work is actually completed and documented.

What this means practically: you may receive an initial payment that’s less than the total repair cost. You do the work, submit final invoices, and then receive the remaining depreciation amount. Make sure you understand which type of coverage you have and how this affects your cash flow during the repair process.

| Florida’s 25% Rule:

The Florida Building Code requires that when more than 25% of a roof is being replaced, the entire roof must be brought up to current code. This is relevant because a claim that starts as a partial repair may become a full replacement once this threshold is crossed, and if your policy covers code compliance upgrades (look for “Ordinance or Law” coverage), that cost may be covered. If your policy doesn’t include this, you’ll be responsible for the upgrade cost. Check your policy and discuss it with your contractor before the adjuster visits. |

Step 4: The Settlement and Getting the Work Done

Once the scope is agreed and the initial payment is issued, work can begin. A few things worth noting at this stage:

Get an itemized written estimate

Not a one-line total, but a line-by-line breakdown of materials, labor, disposal, permits, and any code-compliance work. This protects you, creates a paper trail for the insurer, and makes any supplement claims (additional costs discovered once work begins) easier to substantiate.

Permits are required

In Florida, any roof replacement or significant repair requires a permit. A contractor who suggests skipping this “to save time” is a red flag. Unpermitted work can void your remaining insurance coverage and create problems when you sell.

Supplement claims are common

Once work starts, contractors sometimes discover additional damage that wasn’t visible during the initial assessment, such as rotted decking beneath the tile or water damage to the underlying structure. These additional items can be submitted to the insurer as a supplement claim with documentation. Don’t assume the initial settlement is the only number in play.

Keep all invoices and documentation

Submit them to your insurer promptly when work is complete. This triggers the release of any held depreciation if your policy works on an RCV basis.

| Need an itemized estimate for your claim? Request one from Good Guy Roofing |

Common Mistakes That Cost Florida Homeowners Money

Most claim problems aren’t caused by bad luck; avoidable errors cause them. Here are the ones we see most often.

| Mistake | What it costs you |

| Waiting too long to file | Florida law requires insurers to acknowledge claims within 14 days and resolve them within 90 days, but delayed filing gives insurers grounds to argue the damage worsened due to neglect rather than the storm event. |

| Cleaning up before documenting | Once debris is removed and damaged materials are cleared, the evidence is gone. Document everything first, then clean up. |

| Accepting the first adjuster estimate without review | Adjuster estimates are often conservative, particularly after large storm events when adjusters are overextended. A contractor review frequently identifies scope items that were missed. |

| Signing an Assignment of Benefits (AOB) with a contractor | AOB agreements transfer your insurance rights to the contractor. This is no longer permitted under Florida’s reformed insurance laws, and any contractor asking you to sign one should be a red flag. |

| Not having a contractor present during the adjuster visit | You have the right to have a roofing professional present. Their knowledge of what to look for, and how to describe it, can significantly affect the adjuster’s scope of damage assessment. |

| Using a storm chaser contractor | Unlicensed out-of-state contractors descend on Florida after every major storm. They take deposits, do substandard work, and disappear. Verify any contractor’s Florida licence on the DBPR website before signing anything. |

| Confusing cosmetic damage with covered damage | Insurers in Florida can deny or reduce claims for “cosmetic” damage, meaning damage that doesn’t affect the roof’s function. Understanding this distinction matters for setting expectations. |

| A word on public adjusters:

A licensed public adjuster works on your behalf, not the insurer’s, to assess damage and negotiate your claim. They charge a percentage of the claim settlement, typically 10–20%. In complex or disputed claims, particularly on high-value properties, a public adjuster can be worth that fee. For straightforward claims with a cooperative insurer, they may not be necessary. What they’re not is the same as a contractor, make sure you understand the difference. Having a trusted roofing contractor who can document damage professionally and be present during the adjuster visit often gives you much of the same benefit at no additional cost. |

Realistic Claim Timelines in Florida

One of the most common frustrations homeowners have is that the timeline is longer than they expected. Here’s a realistic picture:

- Days 1–3: Document damage. Call your contractor. File the claim.

- Days 3–14: Insurer acknowledges claim in writing (required by law within 14 days).

- Days 14–30: Adjuster visit scheduled and completed. Longer after major storm events.

- Days 30–45: Scope of loss/estimate received from insurer.

- Days 45–60: Review, dispute if necessary, and agree on scope. Initial payment issued.

- Days 60–90: Work completed, final invoices submitted, recoverable depreciation released (if applicable).

- Days 90+: Full claim closed. Note: Florida law requires insurers to resolve claims within 90 days, though this is frequently extended in the aftermath of large-scale storm events.

If your claim is taking significantly longer than this without clear explanation from your insurer, you have options. Filing a complaint with the Florida Department of Financial Services, or consulting with a public adjuster or insurance attorney, are both legitimate paths if you feel your claim is being unreasonably delayed.

Frequently Asked Questions

Will insurance pay for a roof replacement in Florida?

It depends on why the roof needs replacing. If the cause is a covered peril, most commonly wind or storm damage, and the damage is significant enough to warrant replacement rather than repair, then yes, insurance should cover it, less your deductible. The key variable is the cause. Damage from a named storm, wind event, or falling debris is typically covered. Damage from age, neglect, or gradual deterioration is not. Florida policies also often have a separate hurricane deductible, typically 2–5% of your dwelling coverage, that applies specifically to hurricane-related damage. This is usually higher than the standard deductible, and it catches some homeowners by surprise. Know your deductible before you file.

What roof damage is typically covered?

Wind and storm damage is the most commonly covered category in Florida homeowner policies. This includes damage from named hurricanes and tropical storms, but also from the kind of severe thunderstorms and squalls that move through South Florida regularly. Within that, covered damage typically includes missing or displaced shingles and tiles, flashing damage, structural damage from falling trees or debris, and water intrusion that results directly from storm damage to the roof, not from a pre-existing leak.

What’s generally not covered: wear and tear, cosmetic damage that doesn’t affect function, damage attributable to lack of maintenance, and, in some policies, damage from mould or gradual water infiltration. Florida law introduced restrictions on roof age and coverage in recent years; some policies now limit or exclude coverage for roofs over 15 to 25 years old, depending on the material. This is worth checking on your specific policy.

How long do roof claims take in Florida?

Florida law sets minimum timelines: 14 days to acknowledge a claim, and 90 days to resolve it. In practice, after a major storm event affecting a large area, a category 3 or 4 hurricane, for example, claims can take significantly longer than the 90-day window due to the volume of work adjusters are handling. A straightforward claim on a single-family home after a more localized weather event can often be resolved in 45 to 60 days.

The biggest variables are the volume of claims in your area, the complexity of your specific damage, and whether there’s any dispute about the scope. Having professional documentation and a contractor involved from the start tends to speed things up.

Should I call my roofer or insurance company first?

Your roofer first. The practical reason is that you want a professional damage assessment, documented in writing, before you sit down across from an adjuster. It gives you a clearer picture of your own situation, it gives you professional language to describe the damage, and it means you have someone who can be present during the adjuster visit.

None of this prevents you from filing the claim quickly; you can have your contractor do an assessment and file your claim within a day or two of the storm. You just want to have that professional opinion in hand before the insurer’s person shows up.

Can I choose my own roofing contractor for an insurance claim?

Yes, absolutely. You have the right to choose any licensed contractor you want for the repair or replacement work, regardless of what your insurer suggests or whether they have a “preferred contractor” list. Some insurers do have preferred networks, but participation in those networks is voluntary.

The insurer may want the work estimate to align with their scope and pricing, which is a normal part of the process, but they cannot require you to use a specific contractor. The one caveat: make sure whoever you choose is licensed in Florida (verify on the DBPR website), carries valid liability insurance and workers’ compensation, and can provide references for similar work.

After a major storm, unlicensed out-of-state contractors flood the area. This is not the moment to make a rushed decision on who you hire.

Get in Touch With Good Guy Roofing

The insurance claim process is navigable. It’s not always fast, and it’s not always straightforward, especially in Florida, where the market has become more complicated in recent years. But if you document well, get professional support early, understand your policy before you need it, and avoid the common mistakes, you’re in a much stronger position than most homeowners who go into it blind.

If you’ve just come through a storm and you’re not sure what you’re looking at up on your roof, that’s the right moment to call us. We’ll assess the damage, document it professionally, and walk you through exactly what you’re dealing with before you file anything.

We serve homeowners across Palm Beach County, Broward County, and Miami-Dade County. The assessment is free. The documentation is included. Schedule an inspection for claim support or request a roof repair.